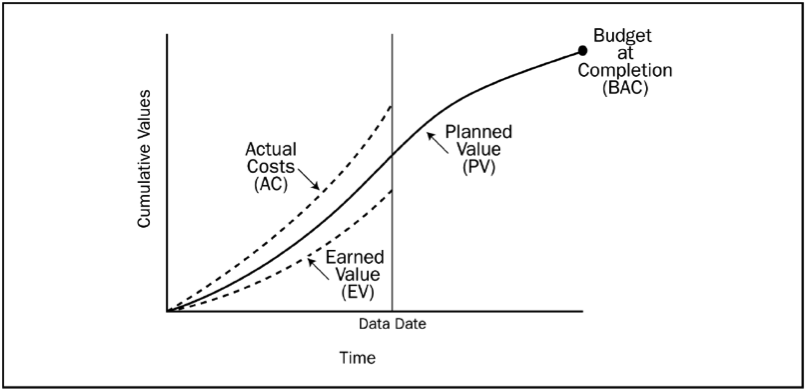

EVM is built on three metrics: Planned value, earned value, and actual cost.

Think of these metrics in terms of your project budget and schedule. Planned value represents how you expect to earn your project budget over the duration of the project. Earned value represents what you actually earn as the project progresses. Actual cost represents what you spend to complete work throughout the project.

At first glance, these terms might seem pretty straightforward, but let’s translate them into even more meaningful terms for a professional services firm.

1. Planned Value = Planned Revenue

Planned value (PV) provides the baseline for tracking project performance in EVM, representing the value a project is expected to deliver over its duration. In the context of consulting projects, PV represents the revenue a project is expected to earn through completion, adding up to the overall project fee or budget. In other words, planned value is planned revenue.

Planned revenue may be expressed as an overall figure for an entire project, or it can be divided across a project’s work breakdown structure (WBS). Additionally, planned revenue can be spread across time periods (e.g., weeks or months), to represent the timing of when a project is expected to earn revenue based on anticipated completion of project deliverables.

2. Earned Value = Earned Revenue

The second metric of EVM is earned value (EV). For design consultancies, this is more aptly termed earned revenue; it represents the revenue a project earns as work is performed and milestones are achieved.

There are multiple ways to earn revenue on a project. Revenue may be earned when the project team charges hours or expenses to the project. Hours charged on a timesheet may be converted into revenue via contracted labor multipliers or bill rate schedules. Expense charges — like travel, printing, or subcontractor expenses — may be converted into revenue via contracted expense multipliers or unit pricing rate schedules.

Revenue may also be earned as project managers assess percent complete across the project WBS. These assessments are often done monthly, and usually stem from progress to-date and how much work remains.

Regardless of how it’s calculated, earned revenue is often governed by planned revenue, which in turn is tied to contract terms. For instance, if the contract dictates a lump sum or fixed fee, earned revenue cannot exceed this amount. A similar limit applies for projects that have cost-plus contracts up to a predetermined maximum amount.

3. Actual Cost = Actual Effort

The final core EVM metric, actual cost (AC), is the market (or retail) value of cost a project incurs as work is performed. This metric provides consultancies with a way to compare how much effort has been expended on a project in relation to the planned revenue and earned revenue on the project. As such, in a professional services context, this metric is better termed actual effort.

In many ways, actual effort accrues on a project similar to the way earned revenue accrues. Actual effort is the result of labor or expense charges being posted to a project, with these charges being converted into actual effort via contracted labor and expense pricing terms.

However, there are two significant differences between actual effort and earned revenue. First, actual effort cannot be calculated or adjusted by percent complete assessments — actual effort is purely a function of the labor or expense charges posted to the project. Second, actual effort is not bound by planned revenue. As your team continues to work on a project, actual effort continues to accrue, even if earned revenue is capped by planned revenue limits.

Another way to understand actual effort comes from its relationship to direct cost. While direct cost represents the cost to a consultancy for services delivered, actual effort represents the market value of services delivered. And while some consultancies may incorporate direct cost into their project management methodology to measure project multipliers or other margin-based metrics, direct cost is not core to EVM.

Closing Thoughts

In order to leverage EVM effectively, a design consultancy must translate EVM’s three core metrics to fit the unique way professional services projects are contracted and delivered. With this understanding, a firm can take the next step of defining additional metrics and thresholds that leverage these core metrics, thus gaining greater insight into project status and enabling early warning indicators of project issues.

I’ll discuss this next step in the third post of this EVM series. In the meantime, please share your EVM questions and/or experiences in a comment below!

Author’s Note: This is the second article in a four-post series on the use of Earned Value Management in professional services organizations.