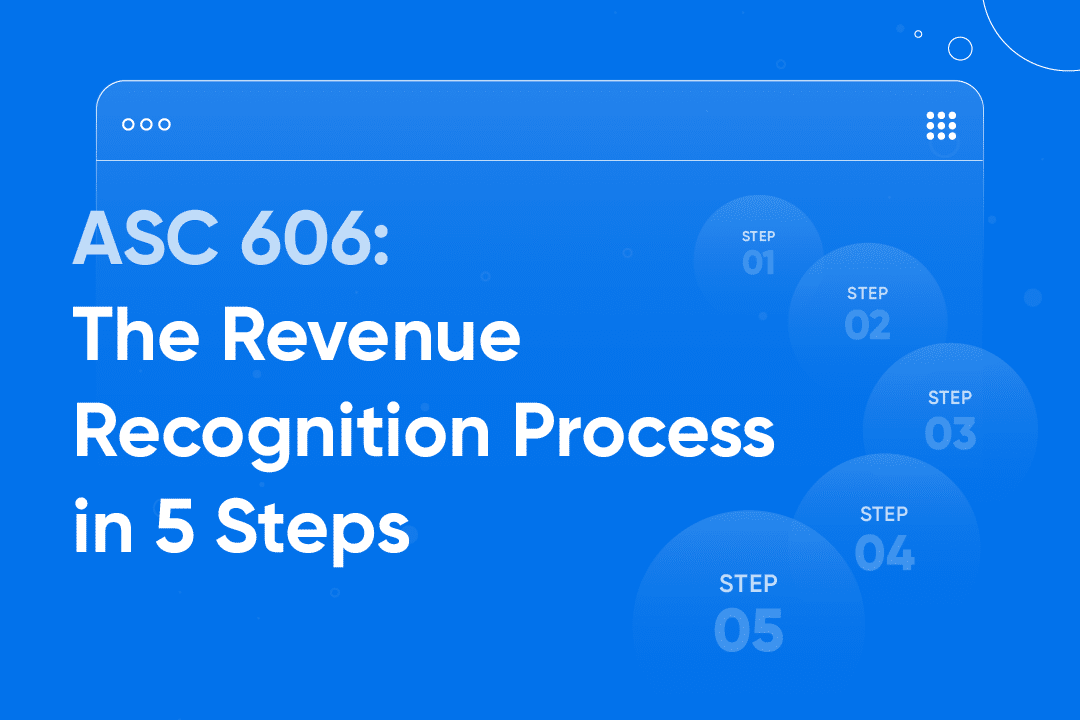

BST Global’s ERP solutions — BST8, BST10 and BST11 — help AEC firms comply with ASC 606, the revenue recognition standard for contracts with customers. ASC 606 has a five-step framework:

- identifying contracts

- defining performance obligations

- determining and allocating transaction prices

- recognizing revenue as obligations are satisfied

BST Global’s ERP solutions include project structures, budgets, fee types, and reporting tools that support each step, providing traceability, accuracy and auditability to simplify compliant revenue recognition.

Simplify ASC 606 Compliance With BST Global’s ERP Solutions

As an AEC firm, your company needs to record and recognize revenue from various contracts. The good news is that BST8, BST10 and BST11 ERP solutions were designed to support the implementation of and be compliant with ASC 606 (known as revenue from contracts with customers).

ASC 606 is the revenue recognition standard that affects all entities — public, private and non-profit — that enter into contracts with clients to provide goods or services.

What are the fundamentals of the ASC 606 accounting standard, and how do BST8, BST10 and BST11 ERP help support them? Essentially, ASC 606 breaks down the revenue recognition process into five steps.

01

Identify the Contract With a Client

ASC 606 states that a firm can account for a contract when all these criteria are met:

- Both parties approve the contract (in writing, verbally or by another agreed-upon method)

- Both parties identify the goods or services to be provided to the client

- Both parties identify and agree on the payment terms

- The contract has commercial substance

- The firm believes it will collect the agreed-upon payment in exchange for providing goods or services to the client

BST8, BST10 and BST11 have ways to record contract details, the work that needs to be performed and how the work will be performed. This happens in the software through the project’s comprehensive work breakdown structure and detailed recordkeeping.

02

Identify the Performance Obligations in the Contract

A performance obligation is the promise to provide goods or services to a client. The firm needs to identify all distinct performance obligations in this firm-client arrangement. A good or service is defined as distinct if:

- The client can benefit from it on its own or with resources the client already has

- It can be provided independent of other performance obligations

Note: Any goods or services that can’t be deemed distinct should be bundled together until they can be.

Performance obligations can also cover an obligation the client might expect because of the client’s history, which can make this part of the process more complex.

Within BST Global’s ERP solutions, the performance obligation can be identified by using the following features:

- Project

- Work breakdown structure

- Budget category (to separate labor, subcontractors and expenses)

- Fee types (denotes the revenue calculation basis, e.g., lump sum, cost plus to a max)

- Revenue variance level

03

Determine the Transaction Price

The transaction price is the amount the firm expects to receive in return for transferring the goods or services outlined in the contract. The amount can be fixed, variable or a combination, but it must be allocated specifically to the performance obligations outlined in step two. Once these performance obligations are fulfilled, the firm can recognize this as revenue.

Within BST Global’s ERP solutions, the billing fee amounts establish the performance obligation price. Typically, the billing fee amounts are clearly traceable back to the signed contract at various project or task levels. These agreed-upon fee types may also be linked directly within your BST Global ERP solution’s budget amounts so that the transaction price is clearly traceable and auditable.

Read more: BST11's Billing App: Eliminate Inefficient Billing Processes & Accelerate Cash Flow

04

Allocate the Transaction Price

If the contract has more than one performance obligation, the firm needs to provide an accurate estimation of that obligation’s standalone selling price versus the total agreed-upon transaction price.

Determining the transaction price allocations can be complicated. Additionally, these allocations can vary based on the aspects of the transaction. ASC 606 includes three methods to determine a performance obligation’s transaction price:

- Expected Cost Plus Margin: This approach considers the forecasted costs of fulfilling the performance obligation and adds margin at the amount the market would be willing to pay.

- Adjusted Market Assessment: This approach considers the market in which the goods or services are sold and estimates the price that a client in that market would be willing to pay.

- Residual: This approach allows a firm that has observable standalone selling prices for one or more of the performance obligations to allocate the remaining transaction price to the goods or services that do not have observable standalone selling prices.

Whichever approach you choose, the standalone selling price must be determined at the outset of the contract (before you initiate the project within your BST Global ERP solution, as you’ll want the budget and fees established at that time).

The standalone selling price should not be updated to reflect changes between contract inception and performance completion (except when there are contract modifications). BST Global’s ERP solutions allow for budgets to be established at the required level of a project’s work breakdown structure for each performance obligation.

05

Recognize Revenue as Performance Obligations Are Satisfied

Performance obligations are considered satisfied when the client obtains control of the asset. The firm can recognize revenue on the performance obligations when the promised good or service is provided to the client. The accounting standard defines methods for recognizing when the control passes at a point in time or over time.

If the obligation is satisfied over time — for example, when project deliverables are completed — the firm needs to decide how to measure the progress and completion of that obligation.

Our ERP solutions use the following to recognize revenue:

- Fee types (including constraints)

- Budgets (effort and cost)

- Calculation of effort when work is performed

- Effort at completion or cost at completion

- Percent complete

All of these work together to support the delivery of the related performance obligations and govern revenue recognition.

Where to Next?

There are many considerations for recognizing revenue. Fortunately, the Association of International Certified Professional Accountants, known as AICPA, has published several guides covering every aspect of this accounting standard. Visit its website for more information.

Please contact your BST Global client manager if you have questions on using our ERP solutions to recognize revenue on your projects under the ASC 606 accounting standard.

Download our ASC 606 compliance ebook now: https://bstglobal.com/bst8-bst10-support-asc-606-compliance-white-paper/